Hidden Value Part 2 - Cogent’s IPv4 Portfolio

This is a follow-up to our prior Insight about Cogent’s hidden asset value. In that post, we discussed the value of Cogent’s portfolio of assets that can and will be monetized over time, primarily through adding new streams of revenue. Within Cogent’s assets is a portfolio of IPv4 addresses that most people (us included) know little about until recently. We’ve been casually watching this market for about two years, ever since we learned that Cogent owned almost 30 million addresses, and we noticed their market values were rising. Their market value suggests there is significant untapped value at the company. Since the company spoke more publicly about these assets on the Q4 call, we have tried to dig deeper and learn more.

This post will summarize what we have learned (so far) about Cogent’s >$2 billion asset portfolio in IP addresses.

Background on IP Addresses

Every device connected to the public internet has a unique IP address. The majority of traffic runs on IPv4 protocols which created 2^32 unique IP addresses, or about 4.3 billion. This repository of addresses was sufficient for decades of global internet growth, but in 2010, the world started running out of them. In 2011, ARIN, one of the global IP address administrators, ran out of available addresses, and other global registries soon followed. It was in 2011 that a landmark transaction occurred, when Microsoft purchased 666,624 IPv4 addresses from Nortel for $7.5 million, or $11.25 per address. Addresses had been freely available from internet registries, but they quickly became scarce and more valuable to private owners.

The proliferation of connected devices over the last twenty years has massively strained global address capacity. Eventually, the world will migrate to IPv6, which is 2^128 or 3.4x10^38 unique addresses. IPv6 has been around since the 1990s, but global compatibility issues and a lack of urgency to move from IPv4 (until the last decade or so) have curtailed the migration of traffic from IPv4 to IPv6.

There are mitigating technologies on IPv4 like Network Address Translation (NAT) which allow for pools of devices to be grouped together on a private IP network, but presented to the world as a single IPv4 address, with NAT devices routing traffic to and from the appropriate end device. This and other techniques have allowed more than 4.3 billion devices to be connected to the public internet, which is how the world has survived on IPv4 thus far. However, there are some downsides to this technique, particularly with regard to security, speed/bottlenecking, and interoperability with other devices on the public internet.

In short, most of the world operates on IPv4, but there are more devices than addresses. Eventually we will move to IPv6, a functionally infinite space with no scarcity of addresses. The timing of that migration is uncertain.

Why haven’t we moved yet? Most devices in the public internet are programmed for IPv4. Some are “dual stack” for IPv4 and IPv6, but the majority of traffic still runs through IPv4 since that is the ubiquitous standard. From our conversations with industry participants, moving to IPv6 requires a comprehensive hardware refresh cycle and a “renumbering” effort which can only be done manually on each device. Above and beyond the hundreds of billions of dollars in equipment capex, there is another several hundred billion dollars of labor costs to renumber those devices. At some point the benefits will outweigh the costs, but in the meantime the mitigation efforts and accessing address capacity from a robust IPv4 leasing and transactional market have been the preferred options.

In 50 years, the world likely will have moved to IPv6. In 10 years, IPv4 will still be around and likely will be carrying significant traffic. These are very imprecise timelines.

Cogent’s IPv4 Portfolio

At recent transaction prices, we can infer that Cogent has over $2 billion of gross asset value in its IPv4 portfolio. In this section, we will walk through how we get to that value.

First, let’s walk through some of the details Cogent shared on its Q4 2023 earnings call:

From its PSINet acquisition, it received 28 million addresses that have been marked at $0 (and still are).

From its recent Sprint acquisition, Cogent received 9.9 million addresses. These were marked at $0 until Q4, when the auditors required the company to report an additional “gain on bargain purchase” of $458 million for these, or roughly $46 per address. Prior to selling Sprint Wireline to Cogent, T-Mobile sold ~2 million of Sprint’s addresses for $121 million (see the footnote below from CCOI’s 8-K on July 17th, 2023) .

The company generates $40 million of run-rate revenue ($35m in 2023 revenue) from leasing 11.4 million of its PSINet IPv4 addresses. It charges $0.30/month and it hasn’t changed its prices since 2015.

See the long quote below for more details from the Q4 call:

“So there’s a fair amount of complexity here. So when we acquired PSINet, we got a large number of addresses previous to Sprint, and we had some organic Cogent and some from other acquisitions. But pre-Sprint, we had approximately 28 million addresses that had 0 value on our balance sheet, yet they had real economic value. Those addresses are traded every day in public exchanges for about $55 an address. You can go online and look at the quotes as we talk. When we did the acquisition of PSINet, there was no value to addresses because they were still available for free. And second, the accounting rules were different, and we recorded things as negative goodwill, which is no longer how you record a gain. You now record it as bargain purchase gain as we did in Sprint’s case.

In the case of Sprint, we acquired 9.9 million incremental addresses, bring our total to about 37.8 million addresses that we own. When that happened, we actually initially were not going to focus on them. And because we have been generating leasing revenue from addresses since 2015, included in our corporate and net-centric numbers, it’s primarily net-centric, it’s roughly 85% net-centric, about almost 13% corporate, and a couple of percent in enterprise. We generate $40 million a year out of leasing those numbers out. We continue to lease out incremental inventory. Today, we are leasing about 11.4 million of the 37.8 million addresses that we currently have. Our average lease price per address is about $0.30 per address per month. We were somewhat unique in the market in having an inventory and being a service provider and leasing these addresses. We didn’t focus a whole lot of attention on it. It was just included in all of our numbers, didn’t even break it out as a separate product. It was just baked in.

Now, we are going to break out the unit count and the number separately. And part of the change occurred about a year ago when Amazon, which had been a serial buyer of addresses, began to compete with Cogent and lease addresses. Amazon leases its addresses on an hourly basis through AWS but nobody really leases them by the hour. And in fact, they generate about $3.60 an address a month, or 12x Cogent’s rate. So based on kind of now a 2-party leasing market and a transaction market, the accounting firm that did the appraisal came back and said, you guys have to recognize a bigger bargain purchase gain to account for these addresses. That’s why we picked up another $254 million.

The final point to this is, we are going to continue to evaluate opportunities to either sell addresses, which we have not done yet, or potentially securitize the cash flows from those addresses. We’re generating about $40 million of EBITDA today off of our address leasing, and that continues to grow. We’ll continue to evaluate. Is it better to lease or should we sell?”

We have tried to assess Cogent’s pool of IPv4 addresses, block by block, to calculate the total portfolio’s value. To do this, we used resources online to find all the IPv4 blocks associated with Cogent’s autonomous system (AS174) and Sprint’s (AS1239). These are the network systems that exchange traffic with the public internet.

IPv4 portfolios are described in block terms. A “/x block” has 2^(32-x) unique addresses. The smaller x is, the larger the block. The largest blocks given to private companies are /8. These have 16,777,216 addresses, and only 6 companies own one of these blocks (per Wikipedia, these are AT&T, Apple, Ford, Cogent, Mercedez-Benz, and Comcast). All the rest are owned by the US government or by the global IP address registries.

In real world terms, owning a /8 block is the equivalent of owning all the real estate in a large MSA like New York, Chicago, LA, San Francisco, etc. A /16 block (65,536 addresses) is like a suburb of the big city. A /24 (256 addresses) is like a neighborhood.

We’ve tried to back into what Cogent has, what Sprint brought to the table, and what the portfolio could be worth. Unfortunately, the publicly available data we have found do not match up perfectly with Cogent’s comments above, but they are close. We calculated Cogent’s portfolio about 39 million addresses in total, with 9.4 million coming from Sprint vs. Cogent’s reporting of 38 million addresses, including 9.9 million from Sprint. We have no doubt Cogent is right, but we’re not sure how to reconcile these numbers from the outside.

The chart below shows our best guess at what Cogent owns, and the estimated price range based on block size. Generally speaking, the larger the block, the more expensive it is.

The massive /8 block from PSINet, the crown jewel in Cogent’s portfolio, is immediately obvious. There are no recent pricing comps for /8, so we simply applied the highest price we found for a /11. Almost certainly the price for a /8 would be higher. We also can see that Cogent has significant scale from /11 to /16 – highly valuable blocks that tend to attract strong demand and prices as well. The pricing curve (derived from IPv4.global’s transaction database) is rather linear and downward sloping, reaffirming larger blocks are more valuable to buyers.

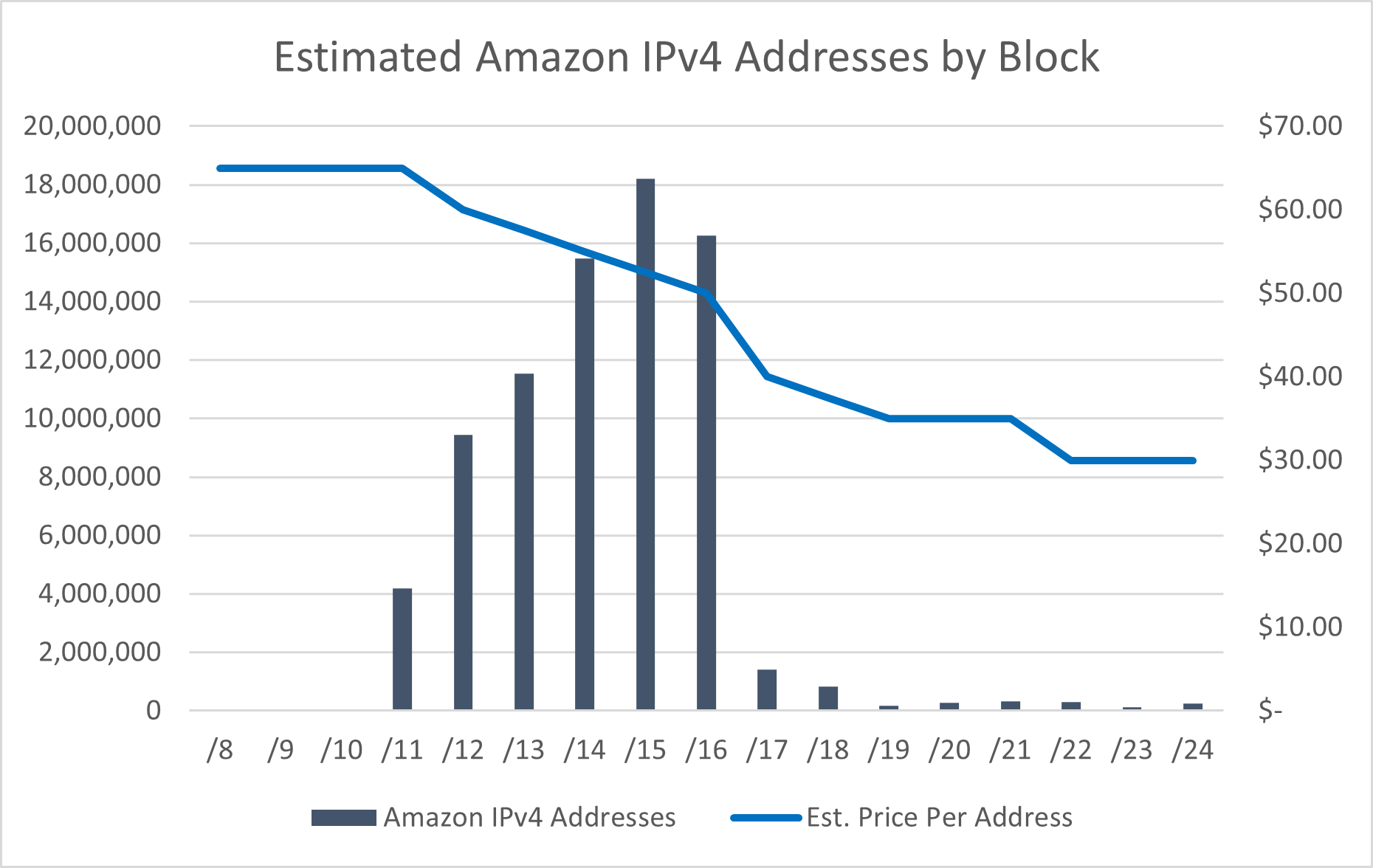

The largest and most dominant buyers in the market in recent years have been hyperscalers – especially Amazon and Microsoft. Both have been very active and have driven most of the purchasing volume in recent years. Using data provided publicly and by some bloggers, we tried to estimate Amazon’s IPv4 address portfolio. Using the same pricing curve as before, we calculate its portfolio value is $4.25 billion.

Amazon has amassed these addresses by buying smaller blocks in the /13 to /16 range, but it has been active everywhere, even down to /24s. Some reports we’ve read suggest that Amazon has about 130 million IPv4s, but the resources we found only showed 78 million. Honestly, it’s a bit hard to know what’s what given all the entities it uses to acquire IPv4 portfolios.

Importantly, large blocks like a /8 can be disaggregated into smaller blocks. For instance, Cogent’s 38.0.0.0/8 could be split into two 38.0.0.0/9 blocks, each of which would have 8,388,608 addresses. It is possible to lease or to sell disaggregated blocks from larger blocks. Disaggregating them provides significant monetization flexibility to registered owners.

Amazon monetizes IPv4 addresses by leasing them to its AWS customers by the hour ($0.005 per hour = $3.60 per month, 12x Cogent’s price). However, AWS also allows customers to BYOIP, i.e. customers with their own IP addresses can put them into their AWS environments and use them without paying the leasing fee. Bringing company-owned IP addresses to a cloud environment adds some operational complexity, but at some scale it likely becomes economically beneficial to do so.

AWS’ BYOIP option and significantly higher lease pricing in the market creates the potential for a nice pricing umbrella for Cogent’s leasing rates and/or inflationary pressure on IPv4 transaction prices. However, since AWS only began charging for IPv4 leasing on February 1, 2024, it is still too early to tell how things will shake out.

How Should Cogent Monetize These Assets?

If the world were to move completely to IPv6 tomorrow, IPv4 addresses would be worth nothing. Therefore, Cogent and all those wishing to monetize IPv4 portfolios should be judicious with their monetization strategies.

Cogent indicated on its Q4 2023 earnings call that it needs “virtually none” (in actuality, 100,000) of its IPv4 address portfolio to run its business. This means it has roughly 37.8 million monetizable addresses.

Currently, Cogent leases 11.4 million addresses which generate $40 million of ARR as of December 2023. From our conversations with the company, these leasing revenues are growing >3% month-on-month and >40% y/y. Per Cogent’s IPv4 leasing guidelines, customers may only lease from Cogent if (a) those addresses are >50% utilized immediately, and (b) >80% are utilized within 3 months. If its leases are not highly utilized, Cogent reserves the right to give the customer a smaller block. The largest block Cogent leases is a /19, or 8,192 addresses, and the smallest is a /24 with 256 addresses.

Because of its stringent requirements for customers to ramp utilization rapidly, it has very little churn: revenue churn is only 0.8% annually despite a weighted-average contract term of 1.5 months. This is a growing and durable stream of recurring revenue which likely will persist for a long time since customers are clearly using all the addresses (per Cogent’s requirements), and clearly they are not renumbering them to IPv6 given the low churn rates. Cogent’s IPv4 leasing customers need more addresses urgently.

We believe the optimal outcome for Cogent to monetize this portfolio involves two paths:

Cogent should continue to grow its IPv4 leasing business with the legacy Cogent portfolio. It clearly has momentum that has been building for years, customer demand is there, and it is a pure-margin stream of revenue. With zero tax basis, any sales from this portfolio would be relatively less efficient.

Within this path, Cogent may pursue securitizations of its leasing revenues to monetize them at attractive rates. For example, perhaps the $40 million of run-rate revenue could be securitized at $350 million of cash to Cogent, with a 6% interest rate. This would be a pretty attractive source of capital – especially because the company has some options to accelerate Sprint synergy realization by buying out bad, uneconomic leases that still have ~3 years of term remaining. With Dave Schaeffer, a hyper-rational capital allocator at the helm, we assume Cogent will consider a securitization only if the use of cash is immediately and obviously accretive.

Also within this path, the company can and should pursue more aggressive go-to-market and pricing techniques to test elasticity of demand and to “sell out” of its leasing space as quickly as possible - possibly even accelerating from >40% annual growth. What was more of a hobby a few years ago has turned into a material growth opportunity given Microsoft’s and Amazon’s push into this market. It’s difficult to know what pricing should be longer term, but it is not crazy to imagine a scenario in which Cogent could lease all of its ~28 million addresses at $0.60/month, or about $200 million of annual revenue. If Amazon’s and Microsoft’s pricing in the market holds, Cogent’s opportunity could be many multiples of this scenario.

We think Cogent should sell the entire Sprint portfolio to a hyperscaler. It might even be able to use this portfolio as one component of a larger deal including significant wavelengths and/or dark fiber, further deepening its relationships with a large and important customer. Cogent’s Sprint IPv4 addresses were marked at $458 million as of Q4 2023, making them the optimal ones to sell to reduce taxable gains. Given the uncertain migration timeline to IPv6 and the inevitable price deflation on IPv4 when that occurs, we think selling a portion of the overall portfolio a good risk-mitigating strategy to pursue, even if it ends up being sub-optimal by not squeezing out every last drop of value. Sprint’s portfolio, on our estimates, should be worth about $500-600 million if we apply the pricing curves above. Cogent has many options for value accretion with that capital.

It is worth noting that this portfolio was a negotiated asset in the transaction with T-Mobile. It is not a pipe dream to value this at $500 million - in fact, that appears to be the negotiated value of it. Without this portfolio, T-Mobile likely would have had to include another $500 million of cash to Cogent, probably through the same Transit Services Agreement (i.e. the TSA would have been $1.2 billion to Cogent instead of $700 million).

Conclusion

This was a pretty lengthy dive into an esoteric portfolio of assets in an unknown and unfollowed corner of the telecom world. Nonetheless, it is a highly valuable and strategic asset to the hyperscalers, who can use their cloud platforms to lease IPv4 addresses at rates far beyond market rates for other owners. This presents an opportunity for Cogent to take advantage of rising demand and rising prices for IPv4 before the inevitable downturn as the internet migrates to IPv6.

We have been tinkering with how to think about the terminal value of IPv4. If we don’t know when the slow migration to IPv6 will render IPv4 much less valuable, how do we value a stream of cash flows from IPv4 leasing? It will be gone in 50 years, but it may be sticky for another 20 or 30 years, and in the near- to medium-term it is growing significantly and has almost no churn. It’s not obvious what the answer is, but we think attributing a discount to Cogent’s overall valuation would be appropriate. Nonetheless, if Cogent can achieve $200 million of IPv4 leasing revenues which trades at 8x, and if it can monetize the Sprint portfolio for $500 million, we still see a path to >$2 billion of enterprise value essentially created out of thin air from Q4 2023’s new disclosures.